As the global race for artificial intelligence supremacy shifts from software algorithms to the physical silicon that powers them, Solstice Advanced Materials (NASDAQ: SOLS) has announced a landmark $200 million expansion of its manufacturing facility in Spokane Valley, Washington. This strategic investment, coming just months after the company’s high-profile spinoff from Honeywell International Inc. (NASDAQ: HON), marks a pivotal moment in the domestic semiconductor supply chain. By doubling its production capacity for critical electronic materials, Solstice is positioning itself as a foundational pillar for the next generation of AI processors and high-performance computing (HPC) systems.

The expansion is more than just a local economic boost; it is a significant case study in the broader trend of semiconductor "onshoring"—the movement to bring critical manufacturing back to United States soil. As the demand for AI-capable chips from industry giants like NVIDIA Corporation (NASDAQ: NVDA) and Advanced Micro Devices, Inc. (NASDAQ: AMD) continues to outpace supply, the Spokane facility will serve as a vital source of sputtering targets, the high-purity materials essential for creating the microscopic interconnects within advanced semiconductors. This move underscores the reality that the AI revolution is as much a triumph of material science as it is of computer science.

Precision Engineering for the Nanoscale Era

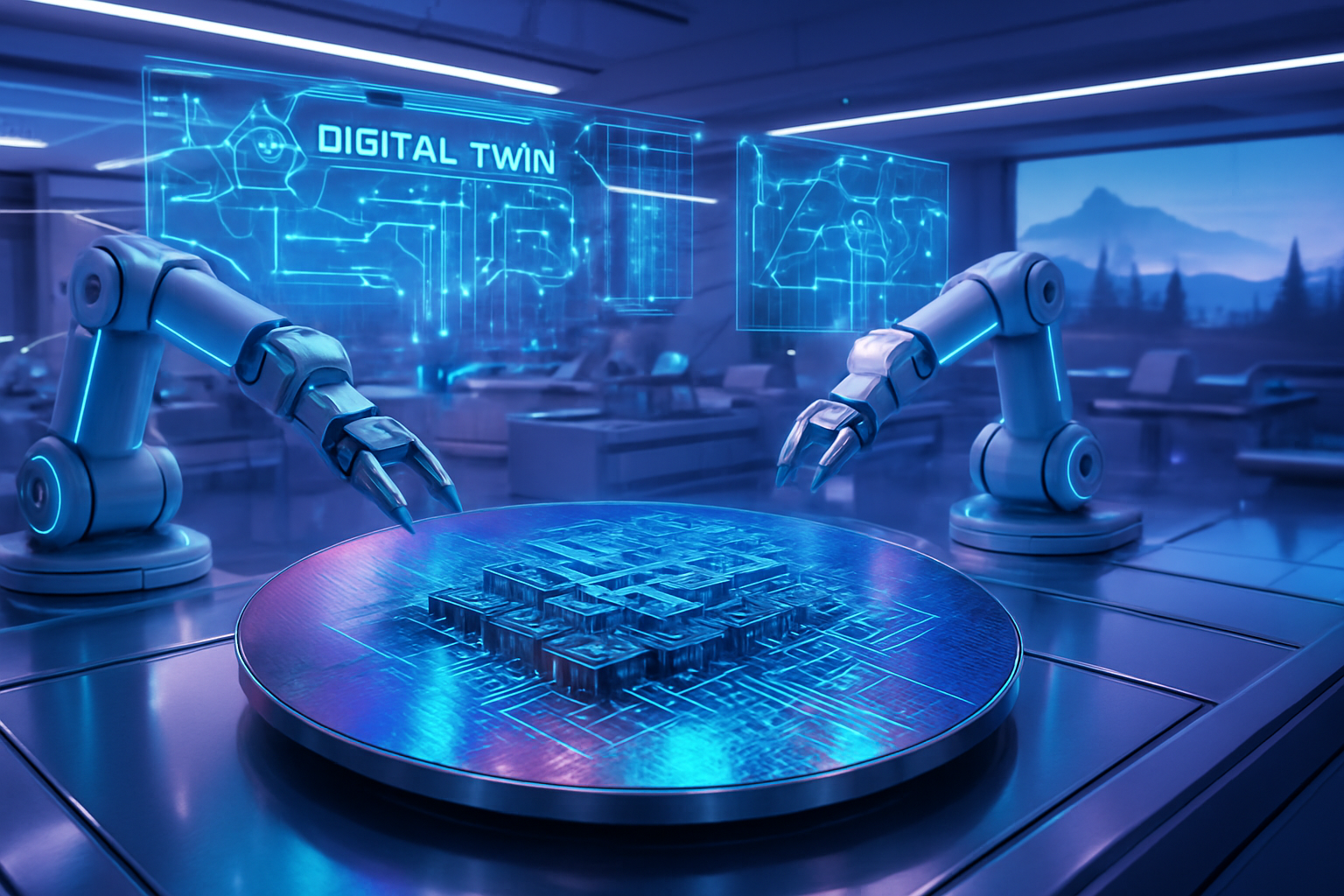

The $200 million project involves a 110,000-square-foot expansion of the existing Spokane Valley site, specifically designed to meet the rigorous standards of sub-5nm chip fabrication. At the heart of this expansion is the production of sputtering targets—discs of ultra-pure metals and alloys used in Physical Vapor Deposition (PVD) processes. These materials are "sputtered" onto silicon wafers to form the conductive pathways that allow transistors to communicate. As AI chips become increasingly complex, requiring denser interconnects and higher thermal efficiency, the purity and consistency of these targets have become a primary bottleneck in chip yields.

Technically, the new facility distinguishes itself through a "Digital Twin" manufacturing approach. Solstice is integrating real-time IoT monitoring and AI-driven predictive maintenance across its production lines to ensure that every target meets atomic-level specifications. Furthermore, the expansion introduces 100% laser-vision quality inspection systems, which replace traditional sampling methods. This shift allows for unprecedented traceability, ensuring that a chipmaker in Arizona or Ohio can trace the specific metallurgical profile of the material used in their most sensitive logic gates back to the Spokane floor.

Initial reactions from the semiconductor research community have been overwhelmingly positive. Materials scientists note that Solstice’s focus on "circular production"—a system designed to reclaim and refine precious metals from spent targets—is a technical breakthrough in sustainability. By recycling used materials directly into the production loop, Solstice aims to reduce the carbon footprint of its Spokane operations by over 300 metric tons of CO2 annually, a move that aligns with the "Green Silicon" initiatives currently trending among major tech firms.

Shifting the Competitive Landscape of Silicon

The strategic implications of this expansion ripple across the entire tech sector. For major chip fabricators like Intel Corporation (NASDAQ: INTC) and Taiwan Semiconductor Manufacturing Company (NYSE: TSM), a robust domestic supply of sputtering targets reduces lead times and mitigates the risks associated with trans-Pacific logistics. In an era where geopolitical tensions can disrupt supply chains overnight, having a "Tier 1" materials supplier within the Pacific Northwest’s "Silicon Forest" provides a significant competitive advantage for U.S.-based manufacturing hubs.

Solstice’s move also puts pressure on international competitors, particularly those based in Asia and Europe. By modernizing its Spokane facility with advanced automation, Solstice is effectively lowering the cost-per-unit while increasing quality, challenging the traditional dominance of overseas suppliers who have historically relied on lower labor costs. For AI startups and specialized chip designers, this expansion means more predictable access to the high-end materials needed for custom AI accelerators, potentially lowering the barrier to entry for hardware innovation.

Furthermore, the spinoff of Solstice from Honeywell has allowed the entity to operate with the agility of a pure-play materials company. This focus is already paying dividends; the company has reportedly secured long-term supply agreements with several "Magnificent Seven" tech companies that are increasingly designing their own in-house AI silicon. By positioning itself as a neutral, high-capacity provider, Solstice is becoming the "arms dealer" for the AI hardware wars.

A Blueprint for Regional Tech Ecosystems

The Spokane expansion is a microcosm of the national effort to rebuild the American industrial base through the lens of high technology. Following the momentum of the CHIPS and Science Act, this project demonstrates how mid-sized cities can become integral nodes in the global AI economy. Spokane’s transformation from a traditional manufacturing town to a high-tech materials hub provides a blueprint for other regions looking to capitalize on the onshoring trend. The injection of $80 million into local Washington-based suppliers alone is expected to create a "multiplier effect," fostering a cluster of specialized logistics, maintenance, and engineering firms around the Solstice campus.

However, the rapid growth of such facilities also brings potential concerns, primarily regarding the "war for talent." With the expansion expected to create over 80 high-tech roles and hundreds of support positions, the local educational infrastructure—including Washington State University and Eastern Washington University—is under pressure to accelerate its semiconductor engineering programs. There are also broader concerns about the environmental impact of chemical processing, though Solstice’s commitment to circular manufacturing and water reclamation has so far mitigated local opposition.

Comparatively, this expansion mirrors the "Gigafactory" model seen in the electric vehicle industry, where vertical integration and local supply chains are prioritized to ensure stability. Just as battery materials were the focus of the 2010s, semiconductor materials are becoming the strategic frontier of the 2020s. The Spokane facility is a clear signal that the U.S. is no longer content to simply design chips; it intends to master the physical substances that make them possible.

The Road to 2029 and Beyond

Looking ahead, the Spokane facility is scheduled to reach full operational capacity by 2029. In the near term, the industry can expect a series of incremental rollouts as new automated lines come online. One of the most anticipated developments is the production of specialized targets for "3D-stacked" memory and logic, a technology essential for the massive bandwidth requirements of Large Language Models (LLMs). As AI models grow in size, the hardware must evolve to include more vertical layers, and Solstice’s new facility is specifically geared toward the materials required for these complex architectures.

Experts predict that Solstice’s success in Spokane will trigger a wave of similar investments across the Inland Northwest. We may soon see a "clustering effect" where chemical suppliers and wafer testing facilities co-locate near Solstice to further minimize transit times. The ultimate challenge will be maintaining this momentum as global economic conditions fluctuate. However, given the seemingly insatiable demand for AI compute, the long-term outlook for the Spokane site remains exceptionally strong.

A New Chapter for the Silicon Forest

The $200 million expansion by Solstice Advanced Materials represents a definitive stake in the ground for American semiconductor independence. By bridging the gap between raw metallurgy and advanced AI logic, the Spokane facility is securing its place in the history of the current technological epoch. It is a reminder that while the "cloud" may feel ethereal, it is built on a foundation of precisely engineered physical matter.

As we move into 2026, the industry will be watching Solstice closely to see if it can meet its ambitious production timelines and if its circular manufacturing model can truly set a new standard for the industry. For Spokane, the message is clear: the city is no longer on the periphery of the tech world; it is at the very center of the hardware that will define the next decade of human innovation.

This content is intended for informational purposes only and represents analysis of current AI developments.

TokenRing AI delivers enterprise-grade solutions for multi-agent AI workflow orchestration, AI-powered development tools, and seamless remote collaboration platforms.

For more information, visit https://www.tokenring.ai/.