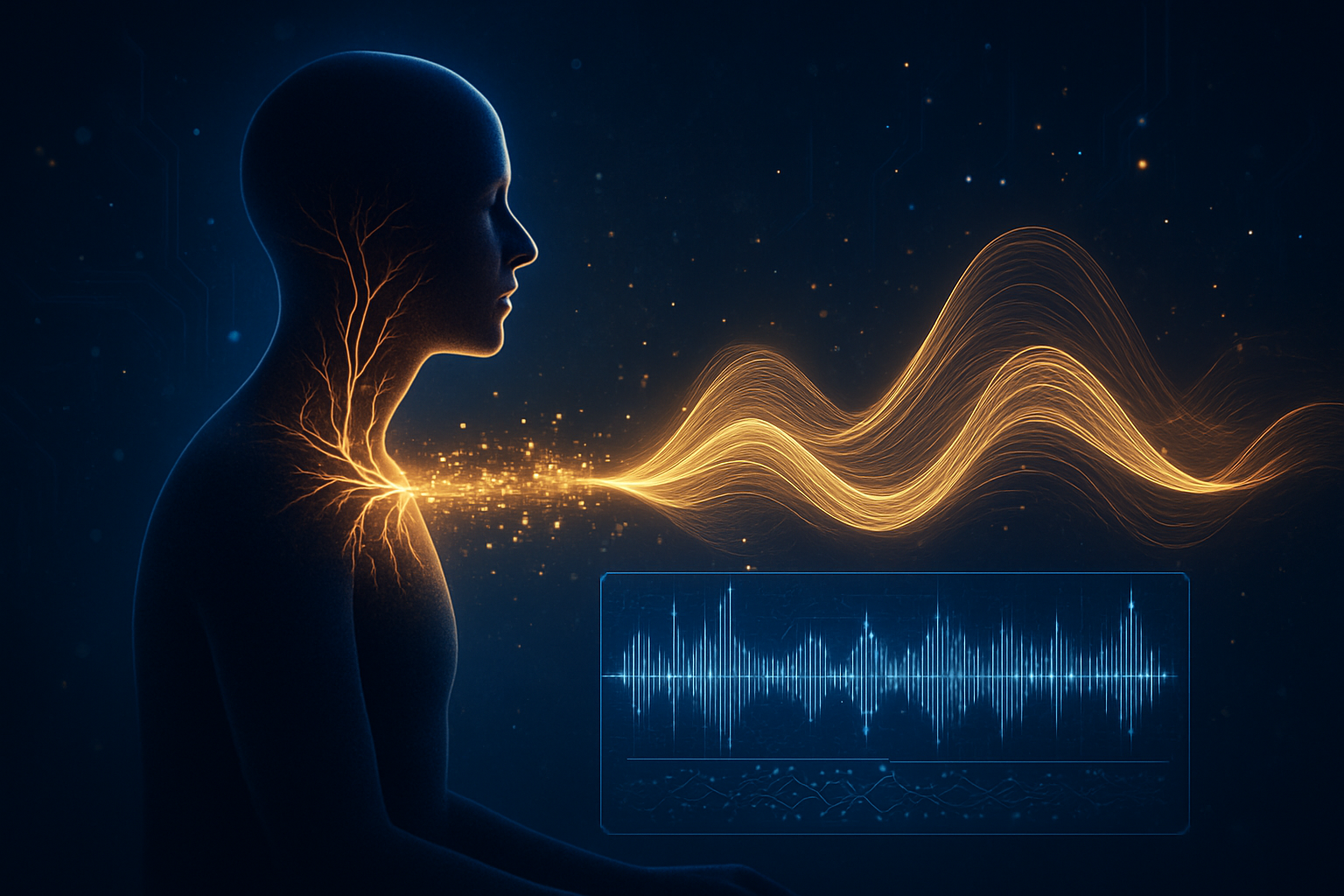

In a landmark shift for assistive technology, ElevenLabs has successfully deployed its generative AI to solve one of the most heartbreaking consequences of neurodegenerative disease: the loss of a person’s unique vocal identity. Through its global "Impact Program," the AI voice pioneer is now enabling individuals living with Amyotrophic Lateral Sclerosis (ALS) and Motor Neuron Disease (MND) to "reclaim" their voices. By leveraging sophisticated deep learning models, the company can recreate a hyper-realistic digital twin of a patient’s original voice using as little as one minute of legacy audio, such as old voicemails, home videos, or public speeches.

As of late 2025, this humanitarian initiative has moved beyond a pilot phase to become a critical standard in clinical care. For patients who have already lost the ability to speak—often due to the rapid onset of bulbar ALS—the ability to bypass traditional, labor-intensive "voice banking" is a game-changer. Rather than spending hours in a recording booth while still healthy, patients can now look to their digital past to secure their vocal future, ensuring that their interactions with loved ones remain deeply personal rather than sounding like a generic, synthesized machine.

Technical Breakthroughs: Beyond Traditional Voice Banking

The technical backbone of this initiative is ElevenLabs’ Professional Voice Cloning (PVC) technology, which represents a significant departure from previous generations of Augmentative and Alternative Communication (AAC) tools. Traditional AAC voices, provided by companies like Tobii Dynavox (TOBII.ST), often relied on concatenative synthesis or basic neural models that required patients to record upwards of 1,000 specific phrases to achieve a recognizable, yet still distinctly "robotic," output. ElevenLabs’ model, however, is trained on vast datasets of human speech, allowing it to understand the nuances of emotion, pitch, and cadence. This enables the AI to "fill in the blanks" from minimal data, producing a voice that can laugh, whisper, or express urgency with uncanny realism.

A major breakthrough arrived in March 2025 through a technical partnership with AudioShake, an AI company specializing in "stem separation." This collaboration addressed a primary hurdle for many late-stage ALS patients: the "noise" in legacy recordings. Using AudioShake’s technology, ElevenLabs can now isolate a patient’s voice from low-quality home videos—stripping away background wind, music, or overlapping chatter—to create a clean training sample. This "restoration" process ensures that the resulting digital voice doesn't replicate the static or distortions of the original 20-year-old recording, but instead sounds like the person speaking clearly in the present day.

The AI research community has lauded this development as a "step-change" in the field of Human-Computer Interaction (HCI). Analysts from firms like Gartner have noted that by integrating Large Language Models (LLMs) with voice synthesis, these clones don't just sound like the user; they can interpret context to add natural pauses and emotional inflections. Clinical experts, including those from the Scott-Morgan Foundation, have highlighted that this level of authenticity reduces the "othering" effect often felt by patients using mechanical devices, allowing social networks to remain active for longer as the patient’s "vocal fingerprint" remains intact.

Market Disruption and Competitive Landscape

The success of ElevenLabs’ Impact Program has sent ripples through the tech industry, forcing major players to reconsider their accessibility roadmaps. While ElevenLabs remains a private "unicorn," its influence is felt across the public sector. NVIDIA (NVDA) has frequently highlighted ElevenLabs in its 2025 keynotes, showcasing how its GPU architecture enables the low-latency processing required for real-time AI conversation. Meanwhile, Lenovo (LNVGY) has emerged as a primary hardware partner, integrating ElevenLabs’ API directly into its custom tablets and communication software designed for the Scott-Morgan Foundation, creating a seamless end-to-end solution for patients.

The competitive landscape has also shifted. Apple (AAPL) introduced "Personal Voice" in earlier versions of iOS, which offers on-device voice banking for users at risk of speech loss. However, Apple’s solution is currently limited by its "local-only" processing and its requirement for fresh, high-quality recordings from a healthy voice. ElevenLabs has carved out a strategic advantage by offering a cloud-based solution that can handle "legacy restoration," a feature Apple and Microsoft (MSFT) have yet to match with the same level of emotional fidelity. Microsoft’s "Project Relate" and "Custom Neural Voice" continue to serve the enterprise accessibility market, but ElevenLabs’ dedicated focus on the ALS community has given it a "human-centric" brand advantage.

Furthermore, the integration of ElevenLabs into devices by Tobii Dynavox (TOBII.ST) marks a significant disruption to the traditional AAC market. For decades, the industry was dominated by a few players providing functional but uninspiring voices. The entry of high-fidelity AI voices has forced these legacy companies to transition from being voice providers to being platform orchestrators, where the value lies in how well they can integrate third-party AI "identities" into their eye-tracking hardware.

The Broader Significance: AI as a Preservation of Identity

Beyond the technical and corporate implications, the humanitarian use of AI for voice restoration touches on the core of human identity. In the broader AI landscape, where much of the discourse is dominated by fears of deepfakes and job displacement, the ElevenLabs initiative serves as a powerful counter-narrative. It demonstrates that the same technology used to create deceptive media can be used to preserve the most intimate part of a human being: their voice. For a child who has never heard their parent speak without a machine, hearing a "restored" voice say their name is a milestone that transcends traditional technology metrics.

However, the rise of such realistic voice cloning does not come without concerns. Ethical debates have intensified throughout 2025 regarding "post-mortem" voice use. While ElevenLabs’ Impact Program is strictly for living patients, the technology technically allows for the "resurrection" of voices from the deceased. This has led to calls for stricter "Vocal Rights" legislation to ensure that a person’s digital identity cannot be used without their prior informed consent. The company has addressed this by implementing "Human-in-the-Loop" verification through its Impact Voice Lab, ensuring that every humanitarian license is vetted for clinical legitimacy.

This development mirrors previous AI milestones, such as the first time a computer beat a world chess champion or the launch of ChatGPT, but with a distinct focus on empathy. If the 2010s were about AI’s ability to process information, the mid-2020s are becoming defined by AI’s ability to emulate human essence. The transition from "speech generation" to "identity restoration" marks a point where AI is no longer just a tool for productivity, but a medium for human preservation.

Future Horizons: From Voice to Multi-Modal Presence

Looking ahead, the near-term horizon for voice restoration involves the elimination of latency and the expansion into multi-modal "avatars." In late 2025, ElevenLabs and Lenovo showcased a prototype that combines a restored voice with a photorealistic AI avatar that mimics the patient’s facial expressions in real-time. This "digital twin" allows patients to participate in video calls and social media with a visual and auditory presence that belies their physical condition. The goal is to move from a "text-to-speech" model to a "thought-to-presence" model, potentially integrating with Brain-Computer Interfaces (BCIs) in the coming years.

Challenges remain, particularly regarding offline accessibility. Currently, the highest-quality Professional Voice Clones require a stable internet connection to access ElevenLabs’ cloud servers. For patients in rural areas or those traveling, this can lead to "vocal dropouts." Experts predict that 2026 will see the release of "distilled" versions of these models that can run locally on specialized AI chips, such as those found in the latest laptops and mobile devices, ensuring that a patient’s voice is available 24/7, regardless of connectivity.

A New Chapter in AI History

The ElevenLabs voice restoration initiative represents a watershed moment in the history of artificial intelligence. By shifting the focus from corporate utility to humanitarian necessity, the program has proven that AI can be a profound force for good, capable of bridging the gap between a devastating diagnosis and the preservation of human dignity. The key takeaway is clear: the technology to "save" a person's voice now exists, and the barrier to entry is no longer hours of recording, but merely a few minutes of cherished memories.

As we move into 2026, the industry should watch for the further democratization of these tools. With ElevenLabs offering free Pro licenses to ALS patients and expanding into other conditions like mouth cancer and Multiple System Atrophy (MSA), the "robotic" voice of the past is rapidly becoming a relic of history. The long-term impact will be measured not in tokens or processing speed, but in the millions of personal conversations that—thanks to AI—will never have to be silenced.

This content is intended for informational purposes only and represents analysis of current AI developments.

TokenRing AI delivers enterprise-grade solutions for multi-agent AI workflow orchestration, AI-powered development tools, and seamless remote collaboration platforms.

For more information, visit https://www.tokenring.ai/.