As of February 2026, the artificial intelligence industry has reached a decisive thermal tipping point. The era of the air-cooled data center, a staple of the computing world for over half a century, is rapidly being phased out in favor of advanced liquid cooling architectures. This transition is no longer a matter of choice or "green" preference; it has become a fundamental physical requirement as the power demands of next-generation AI silicon outstrip the cooling capacity of moving air.

With the widespread deployment of NVIDIA’s (NASDAQ: NVDA) Blackwell-series chips and the first shipments of the B300 "Blackwell Ultra" architecture, data center power densities have skyrocketed. Industry forecasts from Goldman Sachs and TrendForce now confirm the scale of this shift, predicting that liquid-cooled racks will account for between 50% and 76% of all new AI server deployments by the end of 2026. This monumental pivot is reshaping the infrastructure of the internet, turning the quiet hum of server fans into the silent flow of coolant loops.

The 1,000-Watt Threshold and the Physics of Cooling

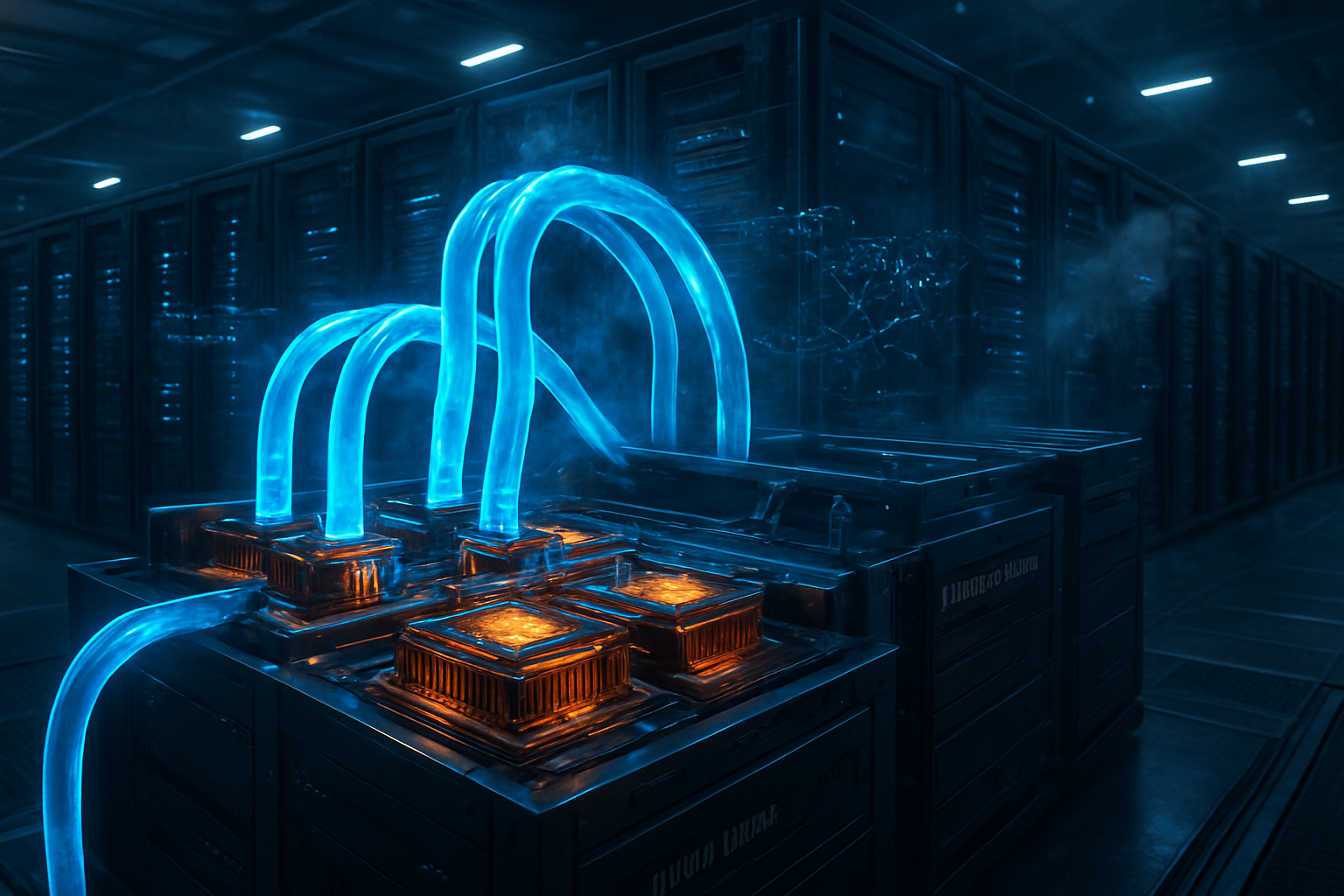

The primary catalyst for this infrastructure revolution is the sheer thermal intensity of modern AI accelerators. NVIDIA’s B200 Blackwell chips, which became the industry workhorse in 2025, operate at a Thermal Design Power (TDP) of 1,000W to 1,200W per chip. Its successor, the B300, has pushed this envelope even further, with some configurations reaching a staggering 1,400W. When 72 of these chips are packed into a single NVL72 rack, the total heat output exceeds 120kW—a density that makes traditional air-cooling systems effectively obsolete.

The technical limitation of air cooling is governed by physics: air is a poor conductor of heat. Research indicates a "hard limit" for air cooling at approximately 40kW to 45kW per rack. Beyond this point, the volume of air required to move the heat away from the chips becomes unmanageable. To cool a 120kW rack with air, data centers would need fans spinning at such high speeds they would consume more energy than the servers themselves and generate noise levels hazardous to human hearing. In contrast, liquid is roughly 3,300 times more effective than air at carrying heat per unit of volume, allowing for a 5x improvement in rack density.

Initial reactions from the AI research community have been pragmatic. While the transition requires a massive overhaul of facility plumbing and secondary fluid loops, the performance gains are undeniable. Industry experts note that liquid-to-chip cooling allows processors to maintain peak "boost" clock speeds without thermal throttling, a common issue in older air-cooled facilities. By bringing coolant directly to a cold plate sitting atop the silicon, the industry has bypassed the "thermal shadowing" effect where air becomes too hot to cool the rear components of a server.

The Infrastructure Gold Rush: Beneficiaries and Strategic Shifts

This transition has created a massive windfall for the "arms dealers" of the data center world. Vertiv (NYSE: VRT) and Schneider Electric (EPA: SU) have emerged as the primary winners, providing the specialized Coolant Distribution Units (CDUs) and modular fluid loops required to support these high-density clusters. Vertiv, in particular, has seen its market position solidify as a leading provider of liquid-ready prefabricated modules, enabling hyperscalers to "drop in" 100kW+ capacity into existing facility footprints.

Server integrators like Supermicro (NASDAQ: SMCI) have also pivoted their entire business models toward liquid-cooled rack-scale solutions. By shipping fully integrated, pre-plumbed racks, Supermicro has addressed the primary pain point for Cloud Service Providers (CSPs): the complexity of onsite installation. This "plug-and-play" liquid cooling approach has given major labs like OpenAI and Anthropic the ability to scale their training clusters faster than those relying on traditional, legacy data center designs.

The competitive landscape for AI labs is now tied directly to their thermal infrastructure. Companies that secured early liquid cooling capacity are finding themselves able to deploy the full power of B300 clusters, while those stuck in older air-cooled facilities are forced to "under-clock" their hardware or space it out across more floor area, increasing latency and operational costs. This has turned thermal management from a back-office utility into a strategic competitive advantage.

Sustainability, Efficiency, and the New AI Landscape

Beyond the immediate technical necessity, the shift to liquid cooling is a significant milestone for data center sustainability. Traditional air-cooled AI facilities often struggle with a Power Usage Effectiveness (PUE) of 1.4 or higher, meaning 40% of the energy consumed is wasted on cooling. Modern liquid-cooled 120kW racks are achieving PUE ratings as low as 1.05 to 1.15. This efficiency gain is critical as the total power consumption of global AI infrastructure is projected to reach gigawatt scales by the late 2020s.

However, the transition is not without its concerns. The primary fear among data center operators remains "the leak." Introducing fluid into a room filled with millions of dollars of high-voltage electronics requires sophisticated leak-detection systems and high-quality materials. Furthermore, while liquid cooling is more energy-efficient, it often requires significant water usage for heat rejection, leading to increased scrutiny from environmental regulators in water-stressed regions.

This milestone is often compared to the transition from vacuum tubes to transistors or the shift from air-cooled to liquid-cooled mainframes in the mid-20th century. However, the scale and speed of this current transition are unprecedented. In less than 24 months, the industry has gone from viewing liquid cooling as an exotic solution for supercomputers to treating it as the baseline requirement for enterprise AI.

The Future: From Cold Plates to Immersion

As we look toward 2027 and beyond, the industry is already preparing for the next evolution: two-phase immersion cooling. While current "direct-to-chip" cold plates are sufficient for 1,400W chips, future silicon projected to hit 2,000W+ may require submerging the entire server in a non-conductive dielectric fluid. This method allows the fluid to boil and condense, utilizing latent heat of vaporization to achieve even higher thermal efficiency.

Near-term challenges include the massive retrofitting required for "brownfield" data centers. Thousands of existing air-cooled facilities must now decide whether to undergo expensive plumbing upgrades or face obsolescence. Experts predict that a secondary market for "lower-tier" AI chips—those under 500W—will emerge specifically to fill the remaining capacity of these older air-cooled sites, while all cutting-edge frontier model training migrates to "liquid-only" facilities.

The long-term roadmap also includes the integration of heat-reuse technology. Because liquid-cooled systems return heat at much higher temperatures (up to 45°C/113°F), it is far easier to capture this waste heat for residential district heating or industrial processes. This could transform data centers from energy drains into municipal heat sources, further integrating AI infrastructure into the fabric of urban environments.

Conclusion: A New Foundation for the Intelligence Age

The rapid transition to liquid cooling marks the end of the first era of the AI boom and the beginning of the "industrial scale" era. The forecasts from Goldman Sachs and TrendForce—placing liquid cooling at the heart of 50-76% of new deployments—are a testament to the fact that we have reached the limits of traditional infrastructure. The 1,000W+ power envelope of NVIDIA’s Blackwell and Blackwell Ultra chips has effectively "broken" the air-cooled model, forcing a level of innovation in data center design that hasn't been seen in decades.

Key takeaways for 2026 include the absolute necessity of liquid-to-chip technology for frontier AI performance, the rise of infrastructure providers like Vertiv and Schneider Electric as core AI plays, and a significant improvement in the energy efficiency of AI training. As the industry moves forward, the primary metric of success for a data center will no longer just be its compute power, but its ability to move heat.

In the coming months, watch for the first announcements of "gigawatt-scale" liquid-cooled campuses and the further refinement of B300-based clusters. The thermal revolution is no longer coming; it is already here, and it is flowing through the veins of the modern AI economy.

This content is intended for informational purposes only and represents analysis of current AI developments.

TokenRing AI delivers enterprise-grade solutions for multi-agent AI workflow orchestration, AI-powered development tools, and seamless remote collaboration platforms.

For more information, visit https://www.tokenring.ai/.