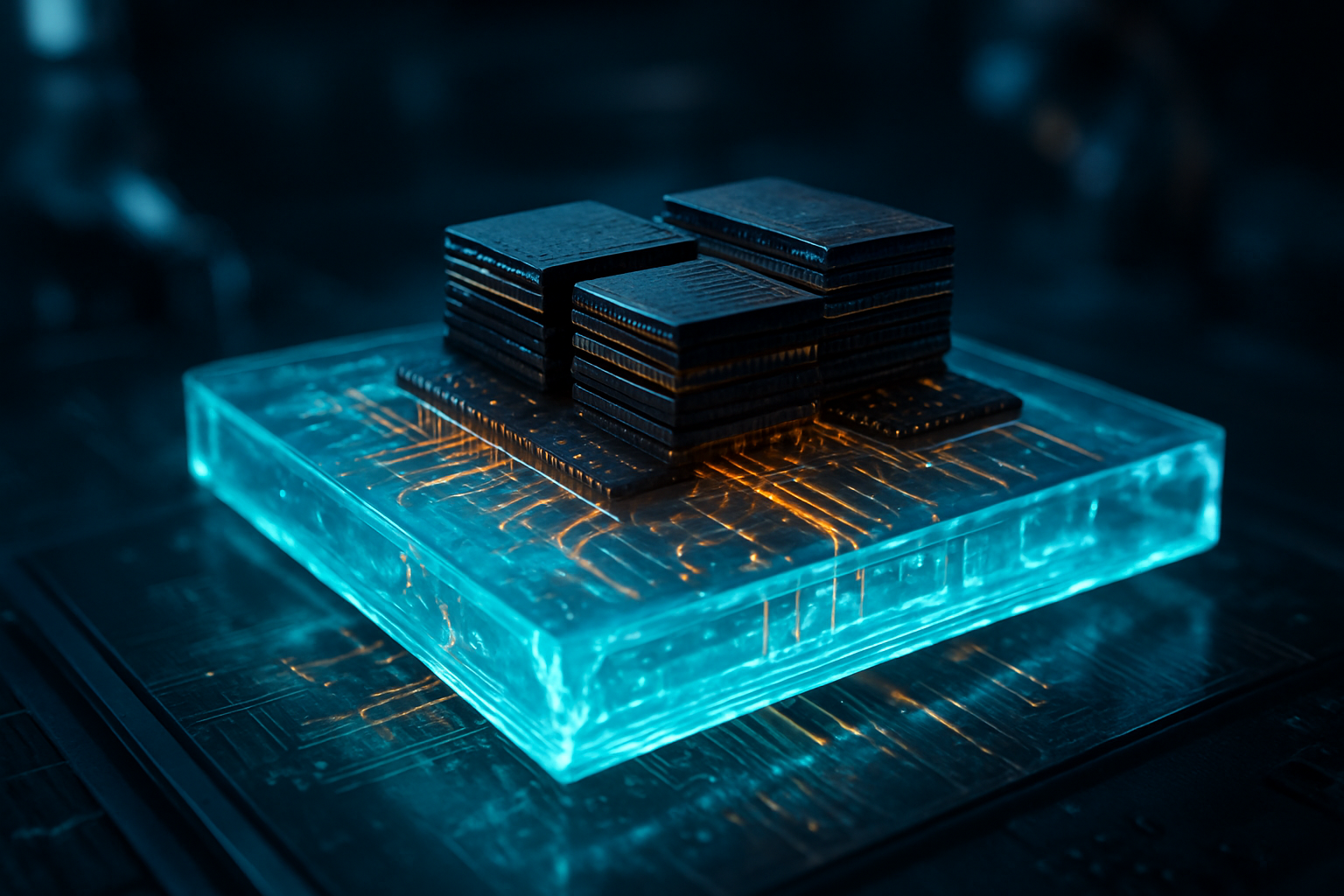

As the demand for generative AI pushes semiconductor design to its physical breaking point, a fundamental shift in materials science is taking hold across the industry. In a move that signals the end of the traditional plastic-based era, industry titans Intel and Samsung have transitioned into a high-stakes race to commercialize glass substrates. This "Glass Revolution" marks the most significant change in chip packaging in over three decades, promising to solve the crippling thermal and electrical bottlenecks that have begun to stall the progress of next-generation AI accelerators.

The transition from organic materials, such as Ajinomoto Build-up Film (ABF), to glass cores is not merely an incremental upgrade; it is a necessary evolution for the age of the 1,000-watt GPU. As of January 2026, the industry has officially moved from laboratory prototypes to active pilot production, with major players betting that glass will be the key to maintaining the trajectory of Moore’s Law. By replacing the flexible, heat-sensitive organic resins of the past with ultra-rigid, thermally stable glass, manufacturers are now able to pack more processing power and high-bandwidth memory into a single package than ever before possible.

Breaking the Warpage Wall: The Technical Leap to Glass

The technical motivation for the shift to glass stems from a phenomenon known as the "warpage wall." Traditional organic substrates expand and contract at a much higher rate than the silicon chips they support. As AI chips like the latest NVIDIA (NASDAQ:NVDA) "Rubin" GPUs consume massive amounts of power, they generate intense heat, causing the organic substrate to warp and potentially crack the microscopic solder bumps that connect the chip to the board. Glass substrates, however, possess a Coefficient of Thermal Expansion (CTE) that nearly matches silicon. This allows for a 10x increase in interconnect density, enabling "sub-2 micrometer" line spacing that was previously impossible.

Beyond thermal stability, glass offers superior flatness and rigidity, which is crucial for the ultra-precise lithography used in modern packaging. With glass, manufacturers can utilize Through-Glass Vias (TGV)—microscopic holes drilled with high-speed lasers—to create vertical electrical connections with far less signal loss than traditional copper-plated vias in organic material. This shift allows for an estimated 40% reduction in signal loss and a 50% improvement in power efficiency for data movement across the chip. This efficiency is vital for integrating HBM4 (High Bandwidth Memory) with processing cores, as it reduces the energy-per-bit required to move data, effectively cooling the entire system from the inside out.

Furthermore, the industry is moving from circular 300mm wafers to large 600mm x 600mm rectangular glass panels. This "Rectangular Revolution" allows for "reticle-busting" package sizes. While organic substrates become unstable at sizes larger than 55mm, glass remains perfectly flat even at sizes exceeding 100mm. This capability allows companies like Intel (NASDAQ:INTC) to house dozens of chiplets—individual silicon components—on a single substrate, effectively creating a "system-on-package" that rivals the complexity of a mid-2000s motherboard but in the palm of a hand.

The Global Power Struggle for Substrate Supremacy

The competitive landscape for glass substrates has reached a fever pitch in early 2026, with Intel currently holding a slight technical lead. Intel’s dedicated glass substrate facility in Chandler, Arizona, has successfully transitioned to High-Volume Manufacturing (HVM) support. By focusing on the assembly and laser-drilling of glass cores sourced from specialized partners like Corning (NYSE:GLW), Intel is positioning its "foundry-first" model to attract major AI chip designers who are frustrated by the physical limits of traditional packaging. Intel’s 18A and 14A nodes are already leveraging this technology to power the Xeon 6+ "Clearwater Forest" processors.

Samsung Electronics (KRX:000660) is pursuing a different, vertically integrated strategy often referred to as the "Triple Alliance." By combining the glass-processing expertise of Samsung Display, the design capabilities of Samsung Electronics, and the substrate manufacturing of Samsung Electro-Mechanics, the conglomerate aims to offer a "one-stop shop" for glass-based AI solutions. Samsung recently announced at CES 2026 that it expects full-scale mass production of glass substrates by the end of the year, specifically targeting the integration of its proprietary HBM4 memory modules directly onto glass interposers for custom AI ASIC clients.

Not to be outdone, Taiwan Semiconductor Manufacturing Company (NYSE:TSM), or TSMC, has rapidly accelerated its "CoPoS" (Chip-on-Panel-on-Substrate) technology. Historically a proponent of silicon-based interposers (CoWoS), TSMC was forced to pivot toward glass panels to meet the demands of its largest customer, NVIDIA, for larger and more efficient AI clusters. TSMC is currently establishing a mini-production line at its AP7 facility in Chiayi, Taiwan. This move suggests that the industry's largest foundry recognizes glass as the indispensable foundation for the next five years of semiconductor growth, creating a strategic advantage for those who can master the yields of this difficult-to-handle material.

A New Frontier for the AI Landscape

The broader significance of the Glass Substrate Revolution lies in its ability to sustain the breakneck pace of AI development. As data centers grapple with skyrocketing energy costs and cooling requirements, the energy savings provided by glass-based packaging are no longer optional—they are a prerequisite for the survival of the industry. By reducing the power consumed by data movement between the processor and memory, glass substrates directly lower the Total Cost of Ownership (TCO) for AI giants like Meta (NASDAQ:META) and Google (NASDAQ:GOOGL), who are deploying hundreds of thousands of these chips simultaneously.

This transition also marks a shift in the hierarchy of the semiconductor supply chain. For decades, packaging was considered a "back-end" process with lower margins than the actual chip fabrication. Now, with glass, packaging has become a "front-end" high-tech discipline that requires laser physics, advanced chemistry, and massive capital investment. The emergence of glass as a structural element in chips also opens the door for Silicon Photonics—the use of light instead of electricity to move data. Because glass is transparent, it is the natural medium for integrated optical I/O, which many experts believe will be the next major milestone after glass substrates, virtually eliminating latency in AI training clusters.

However, the transition is not without its challenges. Glass is notoriously brittle, and handling 600mm panels without breakage requires entirely new robotic systems and cleanroom protocols. There are also concerns about the initial cost of glass-based chips, which are expected to carry a premium until yields reach the 90%+ levels seen in organic substrates. Despite these hurdles, the industry's total commitment to glass indicates that the benefits of performance and thermal management far outweigh the risks.

The Road to 2030: What Comes Next?

In the near term, expect to see the first wave of consumer "enthusiast" products featuring glass-integrated chips by early 2027, as the technology trickles down from the data center. While the primary focus is currently on massive AI accelerators, the benefits of glass—thinner profiles and better signal integrity—will eventually revolutionize high-end laptops and mobile devices. Experts predict that by 2028, glass substrates will be the standard for any processor with a Thermal Design Power (TDP) exceeding 150 watts.

Looking further ahead, the integration of optical interconnects directly into the glass substrate is the next logical step. By 2030, we may see "all-optical" communication paths etched directly into the glass core of the chip, allowing for exascale computing on a single server rack. The current investments by Intel and Samsung are laying the foundational infrastructure for this future. The primary challenge remains scaling the supply chain to provide enough high-purity glass panels to meet a global demand that shows no signs of slowing.

A Pivot Point in Silicon History

The Glass Substrate Revolution will likely be remembered as the moment the semiconductor industry successfully decoupled performance from the physical constraints of organic materials. It is a triumph of materials science that has effectively reset the timer on the thermal limitations of chip design. As Intel and Samsung race to perfect their production lines, the resulting chips will provide the raw horsepower necessary to realize the next generation of artificial general intelligence and hyper-scale simulation.

For investors and industry watchers, the coming months will be defined by "yield watch." The company that can first demonstrate consistent, high-volume production of glass substrates without the fragility issues of the past will likely secure a dominant position in the AI hardware market for the next decade. The "Glass Age" of computing has officially arrived, and with it, a new era of silicon potential.

This content is intended for informational purposes only and represents analysis of current AI developments.

TokenRing AI delivers enterprise-grade solutions for multi-agent AI workflow orchestration, AI-powered development tools, and seamless remote collaboration platforms.

For more information, visit https://www.tokenring.ai/.